A RRIF and a life annuity do not have to be an all-or-nothing decision. Some retirees keep part of their retirement savings in a RRIF for flexibility, while using part to create guaranteed income for life.

Quick Answer

A Registered Retirement Income Fund (RRIF) may be the better option, if access to money and leaving an estate to your beneficiaries are your priorities. A life annuity is the better option if you want a guaranteed monthly income for life and protection against outliving your savings. Many Canadian retirees use a combination of both options.

On This Page

Quick Answer

Turning 71?

RRIF vs. Life Annuity

Understanding Your RRIF Withdrawal Requirements

RRIF Minimum Withdrawal Calculator

When a RRIF May Be Worth Keeping

When a Life Annuity May Be Worth Exploring

You May Be Able to Use Both

Should You Annuitize Your RRIF?

Request a Personal Comparison

Turning 71

By the end of the year you turn 71,your registered retirement savings plan (RRSP) generally needs to be converted into an income option, such as a RRIF or registered annuity. Read: Are You Turning 71?

Your Retirement Income Choices

- RRIF

- Life Annuity

- RRIF and Life Annuity Combination

- Cash Withdrawal

RRIF vs. Life Annuity

| Question | RRIF | Life Annuity |

| Do I keep access to my money? | More access to your savings | No cash access after purchase |

| Who manages the investments? | You manage the investments | Insurance company manages them |

| Can I leave money to beneficiaries? | Remaining funds can be passed on | Depends on options chosen |

| Can I outlive the income? | Yes, can run out | Income lasts for life |

Understanding Your RRIF Withdrawal Requirements

A RRIF requires minimum annual withdrawals. Those required withdrawals generally rise as you get older, which can affect how long your savings remain invested.

RRIF Minimum Withdrawal Rates

| Age At start of year | Annual Minimum Withdrawal (%) 1/(90-age) x 100 |

|---|---|

| 60 | 3.33% |

| 61 | 3.45% |

| 62 | 3.57% |

| 63 | 3.70% |

| 64 | 3.85% |

| 65 | 4.00% |

| 66 | 4.17% |

| 67 | 4.35% |

| 68 | 4.55% |

| 69 | 4.76% |

| 70 | 5.00% |

| 71 | 5.28% |

| View All RRIF Withdrawal Rates | |

RRIF Minimum Withdrawal Calculator

Enter your age to instantly see the minimum percentage you must withdrawal from your RRIF this year.

Calculate Your RRIF Minimum Rate

When a RRIF May Be Worth Keeping

- When you need access to money for emergencies or major expenses

- Leaving an estate to beneficiaries is a priority

- Comfortable managing investments

- Other dependable income from pensions, CPP, OAS or other sources

- You want the potential of investment growth

When a Life Annuity May Be Worth Exploring

- You are concerned about outliving your savings

- Market changes make you uneasy

- You want dependable income for basic monthly expenses

- You want income protection for a spouse

- You prefer less responsibility for managing investments

A combined approach lets you use a life annuity to cover everyday expenses while keeping part of your RRIF available for future needs.

You May Be Able to Use Both

A RRIF can provide flexibility and potential investment growth while a life annuity can help cover essential expenses with income you cannot outlive. Compare RRIFs and Life Annuities

- Guaranteed income for essentials

- RRIF flexibility for emergencies

- No market exposure with a life annuity

- Potential growth with remaining RRIF investments

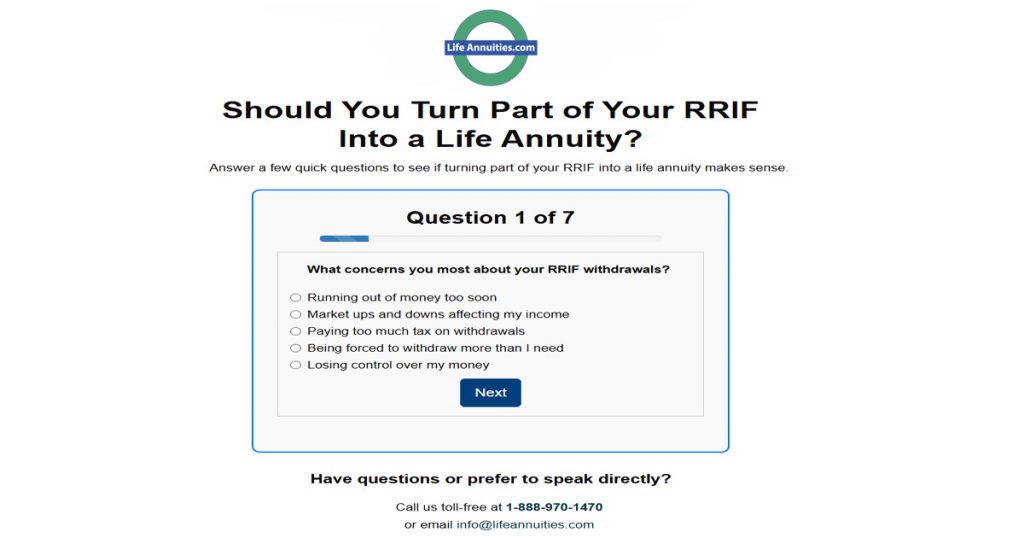

Should You Annuitize Your RRIF?

Answer a few quick questions to see if turning part of your RRIF into a life annuity makes sense. Take the 7-Question RRIF Assessment?

Need a Personal RRIF-to-Annuity Comparison?

An independent financial advisor can help compare a RRIF and a life annuity based on your retirement needs.

Request a Personal Comparison

To review different annuity options use our Annuity Product Finder™. Answer a few quick questions to see which annuity type fits your retirement goals, including joint life, insured annuities, impaired annuities and more.

Disclaimer: This page is for educational purposes and i snot personal financial tax or legal advice.